We earn commissions from brands listed on this

site, which influences how listings are presented.

Last updatedMarch 2026

Our Best Personal Loan Lenders 2026

Get the cash you need, fast

With lower interest rates, you can get the funds you need

while saving thousands on payments. Compare our top personal loans and lock in your rate today.

Our product scores consist of a combination of the

following 3 components:

Popularity

BestMoney measures user engagement based on the number of clicks each listed

brand received in the past 7 days. The number of clicks to each brand will be measured against other

brands listed in the same query. Therefore, the higher the share of clicks a brand receives in any

specific query, the higher the Click Trend Score. BestMoney accepts advertising compensation from

companies, which impacts their (and/or their products’) position, and in some cases, may also affect

their Click Trend Score.

Brand Reputation

Semrush is a trusted and comprehensive tool that offers insights about online

visibility and performance. The BestMoney Total Score will consist of the brand's reputation from

Semrush. The brand reputation is based on Semrush's analysis of clickstream data, which includes

user behavior, search patterns, and engagement, to accurately measure each brand's prominence,

credibility, and trustworthiness. If a brand does not have a Semrush score, the BestMoney Total Score

will be based solely on the Click Trend Score and Products & Features Score (read below).

Features & Benefits

BestMoney’s editorial team researches and reviews financial products based on

factors such as: range of products and services offered, ease-of-use, online accessibility, customer

service, special awards, and more. Each brand is then given a score based on the offerings in each

parameter. The specific parameters which we use to evaluate the score of each product can be found on

its review page.

Personal loans work by letting you borrow a lump sum and repay it in fixed monthly

installments over a set term. In other words, you receive the full amount upfront, then make

scheduled payments that include both principal and interest until the loan is paid off.

How many personal loans can you have at once?

You can have multiple personal loans at once if you qualify for them. Lenders look at your

credit, income, and debt-to-income ratio to decide whether you can manage another loan. Too many

open loans can make approval harder.

What credit score is needed for a personal loan?

Most lenders require a credit score of at least 580. The higher your credit score, the higher

the chance you have to qualify for lower interest rates.

Are personal loans fixed or variable?

Most personal loans are fixed-rate loans. This means your interest rate and monthly payments

remain the same throughout the term. Some lenders offer variable-rate loans, but they are less

common.

Does applying for a personal loan hurt your credit

score?

Applying for a personal loan can temporarily lower your credit score due to a hard credit

inquiry. However, the impact is usually small and short-term. Making on-time payments after

approval can help improve your credit over time.

What Is A Personal Loan?

A personal loan is an installment loan with a fixed interest rate and a fixed monthly

payment, repaid over a set period, typically 2 to 7 years. Banks, credit unions, and online lenders all

offer personal loans, and most are unsecured, meaning they don’t require any collateral.

Unlike many other loan types, you can use personal loans for almost any purpose. That includes

consolidating debt, making large purchases, covering emergency expenses, or paying for events such as a

wedding or a honeymoon.

A personal loan can also be a strategic financial tool. You might use one to replace high-interest

credit card debt with a more affordable monthly payment, build your credit by making consistent on-time

payments, or gain financial breathing room during unexpected situations.

Whether you’re managing medical bills, renovating your home, or streamlining your debts, a personal

loan gives you predictable payments and a clear payoff timeline. Because personal loans are generally

unrestricted, they can be used for almost any major or unexpected expense.

That said, like any kind of financial product, personal loans have trade-offs, including fees and

interest rates, so think carefully before applying for them, since they can impact your credit score.

Key Insights

Personal loans come with fixed monthly payments, which can make it easier to

plan your budget, especially if you’re covering a big expense or combining multiple high-interest

debts into one payment.

Personal loan lenders mostly look at your credit score, income, and existing

debt to decide whether you qualify and what rate you’ll get.

Make sure to shop around, since rates, fees, and service quality vary widely

across direct lenders, credit unions, marketplaces, and P2P platforms.

Other financing options, such as credit cards, HELOCs, and 401(k) loans, may

make more financial sense for your situation, depending on your credit, home equity, and financial

goals.

Always check for hidden fees, compare lenders with soft-pull prequalification,

and choose manageable monthly payments to avoid long-term financial strain.

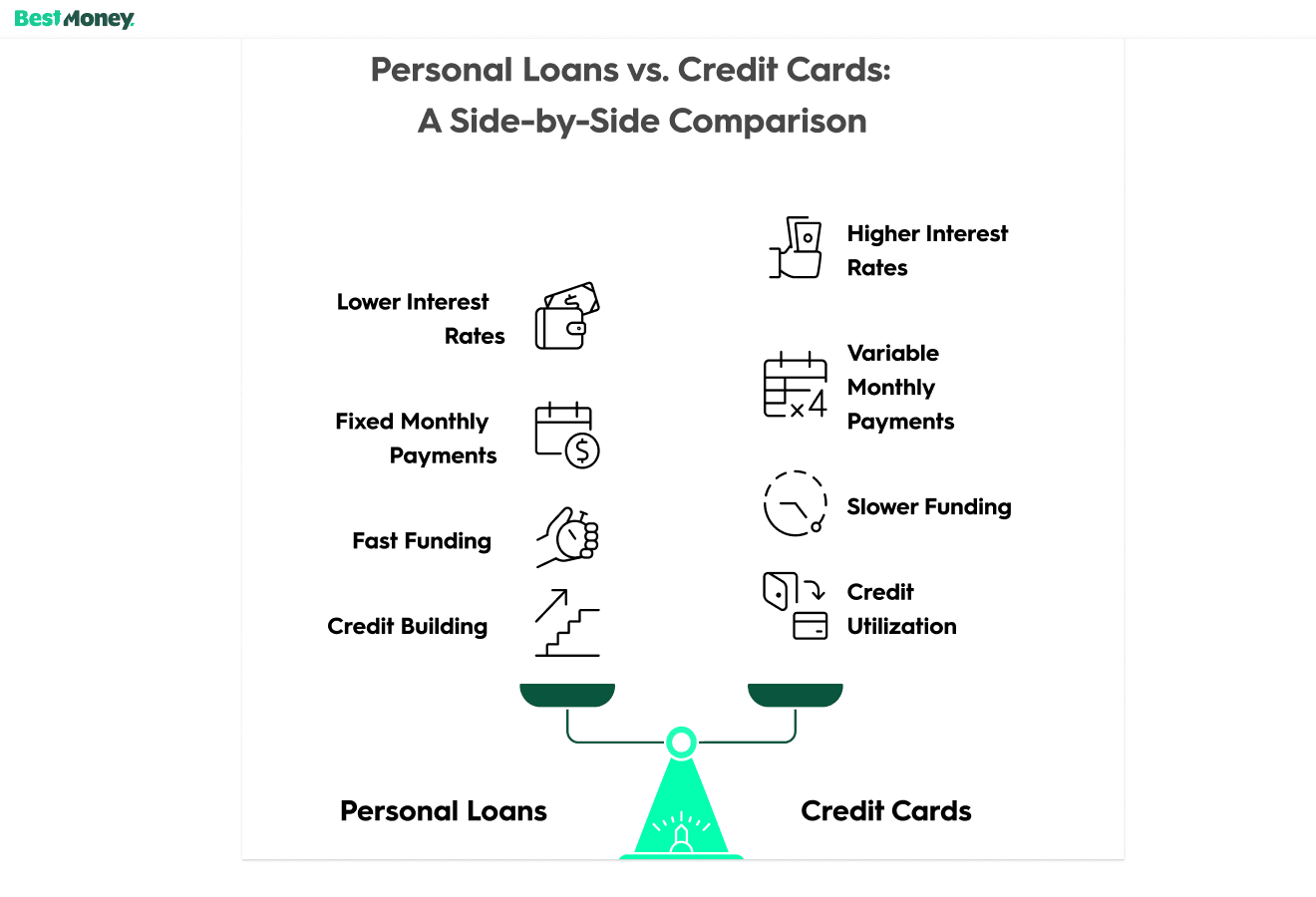

Personal loans offer several advantages over other forms of debt:

Wide range of loan uses: You can use a personal loan for almost anything not

explicitly prohibited by the lender.

Fixed interest rates: Since you pay off a personal loan in installments at a fixed

rate, you’ll have a predictable monthly payment that won’t change for the life of the loan.

Lower interest rates than credit cards: Personal loans often have lower interest

rates, especially for borrowers with good credit. Federal Reserve data shows average credit card APRs around 21% in late

2025, meaning well-qualified borrowers may be able to secure a personal loan at a lower rate and

consolidate debt into a single, predictable monthly payment.

Fast funding: Many personal loan lenders, especially online companies, offer

relatively quick approval and funding timelines. Some can even deliver funds within one business day.

Credit building: Paying off credit cards is a great way to improve your credit

utilization ratio and payment history, both of which play major roles in your credit scores.

What Are The Cons of Personal Loans

Personal loans do come with a few disadvantages, though:

Higher interest rates than secured debt: Mortgages or car loans usually offer lower

rates because they require collateral.

Loan costs: Origination fees, late fees, and other charges can increase the total

cost.

Borrower requirements: You must meet credit and income standards, and lower scores

can lead to higher rates.

Credit risk: Missing payments can damage your credit or even result in legal

action.

Inflexible payment schedule: Once you choose the amount you want to take out and

your repayment term, you’re locked into that payment schedule until the repayment period ends.

What Are The Borrower Requirements For Personal Loans?

When you apply for a personal loan, lenders evaluate your financial profile to determine whether you

qualify and what interest rate you’ll receive. Understanding how to qualify for a personal loan can help

you strengthen your application and improve your approval chances. This typically includes a credit

check and a detailed review of the information in your application.

Here are the main factors lenders look at:

Credit Score

Your credit score is one of the biggest influences on your approval odds and the interest rate you’re

offered. Some lenders set minimum credit score requirements, while others are more flexible. But according to Experian, most lenders prefer a

credit score of at least 580. Strong credit usually leads to better rates, while lower scores may limit

your options or result in higher borrowing costs.

Expert Tip: Instant Approval Is a Red Flag

“Instant Approval and No Credit Check claims should be avoided at all

costs. If it sounds too good to be true, it probably is! Also, loans that require no credit check

are almost always going to come with undesirable terms that are buried in the contract fine print.”

Eric CloakCFP

and President atCroak Capital

Income

Lenders verify your income to ensure you can comfortably afford your loan payments. The higher your

income, the more likely you are to qualify for the loan amount you’re requesting. You may be asked to

provide pay stubs, tax documents, or other proof of earnings.

Debt-to-Income (DTI) Ratio

Your DTI ratio compares how much you owe each month to how much you earn. For example, if you earn

$5,000 a month before taxes and pay $2,000 toward debts, your DTI ratio is 40%. The higher that

percentage, the less room there is in your budget for additional payments.

If a large percentage of your income already goes toward debt payments, lenders may see you as a higher

risk and decline your application or offer a smaller loan amount.

Loan Amount and Loan Term

The loan amount and the length of your repayment term also factor into the approval decision. A larger

loan or a longer repayment period can increase the lender's risk, leading to higher rates or

stricter approval criteria.

Finding the right personal loan starts with a reality check on your finances. Think about how much you

need to borrow, how quickly you want the money, and what kind of monthly payment is realistic for your

budget. If you have a solid credit score, steady income, and manageable debt, many lenders will be

willing to work with you.

If you prefer working with a familiar institution or want help face-to-face, consider traditional banks

and credit unions that offer in-person service and strong reputations. But keep in mind that their

approval processes can be slower.

Online lenders are built around speed and ease of use. Many let you check potential rates in minutes,

complete the entire application online, and access funds in as little as one business day.

Start by Shopping Around

Many financial experts recommend comparing several lenders instead of going with the first offer you

see. Rates, fees, and approval requirements can vary widely, so you’ll want to cast a wide net before

committing to one. You can also use prequalification tools, available on most lender websites, to check

estimated rates without affecting your credit score.

Loan marketplaces are another useful option, since they let you compare offers from several lenders

using a single application.

What to Look For When Comparing Lenders

Here’s what you want to pay attention to when you’re comparing lenders.

Interest rate: This is the biggest factor affecting the total cost of your loan. A

lower rate means you’ll pay less over time.

Loan fees: Lenders may charge origination fees, late fees, processing fees, or

prepayment penalties. Origination fees are deducted from your loan amount upfront, so you should

factor them into how much you need to borrow.

Loan amounts: Each lender offers its own minimum and maximum loan amounts. Make

sure the lender supports the amount you need.

Loan terms: Repayment periods vary widely. Shorter terms mean higher monthly

payments but less total interest. Longer terms lower your monthly payment but cost more overall.

Monthly payment: Choose a payment that comfortably fits into your budget. If the

payment feels tight, the loan may not be the right fit.

Consumer reputation: Look at reviews on Trustpilot, the Better Business Bureau, and

government resources like the Consumer Financial Protection Bureau. Pay attention to recurring

complaints about customer service, billing errors, or unexpected fees.

Make Sure the Lender is Legitimate

Before accepting a loan offer, review the lender’s background. Look for signs of reliability, such as:

A long history of operating in the lending industry

Positive customer reviews

Clear and transparent terms

Responsive customer service

No pattern of complaints or legal issues

You should feel confident that the lender is reputable and operates with integrity.

Expert Tip: Clarity Before Commitment

“If you can’t understand something, and it is not easily explained, be

very cautious before you move forward. Very often, bad actors in the financial space will say one

thing, but a totally different thing is in the documents you are signing. That’s when you know it is

time to walk away and not do business with them.”

Bobbi RebellCFP® and Personal Finance Expert atFinancial Wellness Strategies

Alternatives To Personal Loans

A personal loan isn’t the only way to cover a major expense or manage your finances. Depending on what

you need the money for, how quickly you need it, and what assets you have available, one of these

alternatives may offer lower costs or more flexibility.

Credit Cards or Personal Lines of Credit

If you need spending flexibility instead of a one-time lump sum, a credit card or personal line of

credit can fill that gap.

A credit card is a payment card that lets you make purchases online and in-store. When you use it to

pay for goods or services, you essentially authorize the credit card company to make the purchase for

you, with the promise to pay the exact amount back at a later date.

The main drawback is cost. Recent analysis from the Consumer Financial Protection Bureau shows

that average APRs on credit card accounts assessed interest have climbed to roughly the low‑20% range

and are at their highest levels since data collection began.

These rates are typically higher than what well‑qualified borrowers pay on personal loans, and most

cards have variable APRs, which can make monthly payments harder to predict. To avoid long‑term credit

card debt, it’s best to reserve cards for smaller or unpredictable expenses and pay balances off

quickly.

If you’re a homeowner and have enough equity built up, you may be able to borrow at lower rates by

using your home as collateral. Here are two ways to do that:

Home equity loans provide a fixed-rate lump sum, ideal when you already know the

full cost of your project or expense.

HELOCs offer a revolving line of credit backed by

your home’s value, giving you ongoing access to funds.

Because these options are secured by your property, they often come with better pricing, but also

greater responsibility since your home is on the line.

401(k) Loans

If your employer’s retirement plan allows it, borrowing from your 401(k) can provide fast funding

without a credit check.

With 401(k) loans, you repay yourself with interest, and payments are usually deducted from your

paycheck. This can be a lower-friction option when cash is tight.

That said, it comes with tradeoffs. While the loan is outstanding, that money isn’t invested, which can

slow your retirement growth. And if you leave your job before the loan is fully repaid, the remaining

balance can be treated as a distribution, which could then trigger income taxes and early withdrawal

penalties.

The Types of Personal Loans

Personal loans come in a few main forms. Understanding the differences can help you choose the option

that best fits your needs and budget.

1. Unsecured vs. Secured Loans

Unsecured loansare the most common. They don’t require collateral, but often come with higher rates and

stricter credit requirements.

Secured loansuse an asset, such as

a car or a savings account, as collateral. They typically offer lower interest rates, but put your

asset at risk if you can’t make payments.

2. Peer-to-Peer (P2P) Loans

These loans are funded by individual investors through online platforms. They can be useful if you have

average credit or prefer a fully online process, though rates and fees vary widely.

3. Fixed-Rate vs. Variable-Rate Loans

Fixed-rate loans lock in your interest rate and monthly payment.

Variable-rate loans start lower but can rise or fall with market conditions. They

may make sense if you plan to repay quickly.

4. Lines of Credit

A personal line of credit gives you ongoing access to funds that you can draw from as needed. The key

difference in a personal loan vs. a line of credit is that a personal loan gives you a lump sum, while a

credit line lets you borrow only what you need over time. You’ll only pay interest on what you borrow,

but rates are usually higher than standard personal loans.

5. Signature Loans

An unsecured “signature loan” is approved solely based on your credit profile. No collateral is

required, but interest rates may be higher.

6. Cash Advances & Balance Transfers

Cash advances let you borrow against your credit card’s limit, but often come with

steep fees and high interest.

Balance transfers allow you to move credit card debt to a card with a low or 0%

introductory APR—helpful if you can repay before the promo period ends.

Personal loans fall under this category: fixed payments over a set schedule. Other examples include

auto loans and mortgages.

What To Know Before Applying For A Personal Loan

Before you submit a personal loan application,

make sure you know what you’re getting into. When you understand the loan process and what to look for,

it’s easier to secure better rates, avoid unnecessary fees, and increase your chances of approval.

Check Your Credit Profile

Your credit report tells you more than just your score. Reviewing it beforehand allows you to:

Catch errors that could lower your score

Understand how lenders will view your credit health

Identify areas you may want to improve before applying

You can get free annual reports from major credit bureaus at annualcreditreport.com, and many banks now offer credit score updates at

no cost. Some borrowers note that applying alone rather than jointly can result in better terms if one

applicant has much stronger credit.

Compare Interest Rates and APRs

Understanding how personal loan interest works helps you compare offers more accurately and avoid

unnecessary costs. When you’re comparing your options, look for:

Competitive fixed rates

Transparent APRs

No hidden or unnecessary charges

Note that a loan's interest rate doesn't include loan fees, whereas the APR tells you the

full cost you'll pay to borrow on an annual basis, including fees.

Review Your Monthly Budget

Before applying, estimate how much you can comfortably afford each month. You’ll want a payment that

fits your budget without straining your finances. If you haven’t already, create a detailed budget

before applying so you know whether you can actually afford to take out a personal loan.

Decide How Much You Actually Need

Borrowing more than necessary increases your costs. Determine your exact funding needs and look for a

loan amount that matches them without forcing you into a higher monthly payment.

Choose the Right Loan Term

Short-term financing means higher payments but lower interest costs. Long-term offers lower monthly

payments but increase the total amount you repay. Your ideal term depends on:

Your cash flow

Your budget

How quickly do you want to be debt-free

Understand Fees Upfront

Before applying, check whether your lender charges:

Origination fees

Late fees

Prepayment penalties

Processing or administrative fees

You’ll also want to double-check for hidden fees or early repayment penalties, particularly with

subprime lenders.

A government-issued photo ID, such as a driver’s license or passport

Proof of income, like recent pay stubs, tax returns, or bank statements

Proof of residence, such as a utility bill or lease agreement

Employment information, including your employer’s name and contact details

Bank account information for funding and monthly payments

Some lenders may also request additional documentation, especially if you’re self-employed or have

irregular income.

Applying For An Online Personal Loan

Applying for a personal loan with an online lender is typically faster compared to going through a

traditional bank. The application process is typically straightforward and consists of three stages.

Stage 1: Initial Application

You complete a short online form with basic information, including:

Desired loan amount

Purpose of the loan

Personal details (name, address, contact info)

Income and employment information

Housing status

This takes only a few minutes and helps the lender understand your financial profile.

Stage 2: Soft Credit Check & Prequalification

The lender runs a soft credit check, which doesn’t affect your credit score. Based on your information

and credit profile, you’ll receive:

A potential loan amount

Estimated interest rates

Repayment term options

Prequalification lets you compare offers without committing.

Stage 3: Full Application & Verification

If you move forward, the lender:

Performs a hard credit inquiry

Requests supporting documents such as:

Government-issued ID

Proof of income (pay stubs or bank statements)

Proof of residence

After verification, many lenders provide same-day approval and can deposit funds into your bank account

within 1 to 2 business days. In many cases, the entire process can take as little as one

business day.

What Are The Different Types of Lenders?

You can get a personal loan from several types of

lenders, and each comes with its own pros, requirements, and application process. Knowing how they

differ can make it easier to find the right fit.

Direct Lenders

These are banks, credit unions, and online lenders that issue loans directly to you.

Faster decisions than traditional banks (especially online lenders)

Clear and upfront communication, since you’re dealing with one institution

A good choice if you want a straightforward borrowing experience

Loan Marketplaces

Marketplaces let you compare offers from multiple lenders in a single application.

Helpful for rate shopping

No need to fill out multiple forms

Often provides a wide range of loan options, from prime to subprime

Peer-to-Peer (P2P) Lenders

P2P platforms connect borrowers with individual investors who fund the loans.

Useful if you have average or fair credit

Fully online application process

Rates and fees vary based on risk level and platform policies

Banks

Traditional banks offer personal loans, but often have stricter qualification requirements.

Best for borrowers with strong credit and steady income

Can offer competitive rates for well-qualified applicants

Approval and funding may take longer than with online lenders

Personal Loan Glossary

APR (Annual Percentage Rate): The total yearly cost of a loan, including interest

and applicable fees. It gives you a clearer picture of what you’ll pay, rather than just the interest

rate alone.

Debt-to-Income Ratio (DTI): The percentage of your monthly income that goes toward

debt payments. Lenders use this number to understand how much additional debt you can handle.

Fixed Interest Rate: An interest rate that stays the same for the entire loan term,

keeping your monthly payments stable.

Variable Interest Rate: An interest rate that can rise or fall based on market

conditions. Your monthly payment may change over time.

Loan Term: The amount of time you have to repay your loan. Terms commonly range

from 12 to 84 months.

Origination Fee: A one-time fee some lenders charge to process your loan. It’s

usually deducted from your loan amount.

Principal: The original amount you borrow before interest and fees are added.

Prepayment Penalty: A fee charged if you pay off your loan early. Not all lenders

charge this.

Soft Credit Check: A credit inquiry that doesn’t impact your credit score. Used for

prequalification.

Hard Credit Check: A credit inquiry that can temporarily lower your credit score.

Performed during a full loan application.

Secured Loan: A loan backed by collateral, such as a car or savings account. It can

offer lower rates but carries more risk if you can’t repay.

Unsecured Loan: A loan that doesn’t

require collateral. Approval depends on your credit, income, and financial history.

Underwriting: The process lenders use to review your application and decide whether

to approve your loan.

Installment Loan: A loan repaid in regular and fixed payments over a set period.

Personal loans fall into this category.

Comparing The Best Personal Loans

Company

Loan Type

Credit Profile

Notable Features

LendingTree

Marketplace

Broad Credit Range

Single application with access to multiple lender offers

SoFi

Unsecured Personal Loan

Good to Excellent

No origination fees, clear fee structure, and member benefits

Credible

Marketplace

Fair to Excellent

Soft credit check with side-by-side rate comparisons

AmeriSave Mortgage

Secured Loan / Mortgage Products

Good to Excellent

Home-secured borrowing options with competitive pricing

LightStream

Unsecured Personal Loan

Excellent

No fees, high loan limits, flexible loan purposes

Best Egg

Unsecured Personal Loan

Fair to Good

Flexible terms, commonly used for debt consolidation

Figure

HELOC

Good to Excellent

Fully digital application with fixed-rate draw options

MoneyLion

Personal Loans & Cash Advances

Fair to Poor

Credit-building tools alongside loan access

Happy Money

Unsecured Personal Loan

Fair to Good

Focused on credit card payoff and borrower-friendly terms

What The Community Is Saying (Based on Reddit Discussions)

This section summarizes common themes from public Reddit discussions about choosing a personal loan

lender. It reflects aggregated community sentiment rather than individual opinions, endorsements, or

provider claims.

Across discussions, users tend to prioritize transparency, flexibility, and overall fit over

promotional offers. Many emphasize evaluating how lenders handle the full process—from application to

repayment—rather than focusing only on advertised interest rates.

Interest rates matter, but context is key. Reddit users often recommend comparing

multiple lenders, particularly credit unions and local banks, which are frequently viewed as offering

more competitive and flexible terms. At the same time, they caution against “guaranteed approval”

offers, which are commonly associated with higher costs.

Fees and total borrowing cost are frequent pain points. Origination fees and unclear

charges are frequently mentioned, prompting users to stress the importance of carefully reviewing

disclosures and checking third-party reviews for recurring issues.

Eligibility requirements strongly affect outcomes. Community discussions consistently

note that credit score, income stability, and debt-to-income ratio influence approval odds and loan

terms, with stronger profiles generally receiving better offers.

Customer service becomes more important after approval. Beyond rates and fees, users

value responsive support and clear communication once the loan is active, particularly when questions or

problems arise.

In summary, Reddit discussions suggest the best personal loan lender is highly

situational. Users repeatedly recommend comparing options, understanding the full cost of

borrowing, and choosing a lender whose terms and service model align with your financial situation.

Compare With

BestMoney.com, Choose the Best for You

At BestMoney.com, we

understand the importance of making informed financial decisions. Our team of financial experts and

editors conducts thorough research across lending, banking, home loans, personal finance, and

insurance to provide you with comprehensive comparisons and insights. We continuously update our

content to reflect the latest market trends and offerings, ensuring you have access to current,

reliable information.

We offer a wide range of

services, including detailed comparison tools and expert reviews, all designed to meet your specific

financial needs. Our mission is to empower you to make confident, well-informed choices that help you

achieve your financial goals.

Methodology: How We Evaluated Personal Loan Lenders

To determine the best personal loan lenders, we evaluated providers across key criteria that influence

cost, eligibility, flexibility, and overall borrower experience. Our goal was to highlight lenders that

offer transparent terms, reasonable costs, and reliable support across a range of credit profiles.

Our analysis is based on publicly available information, third-party reviews, and summarized consumer

sentiment research. All rankings and “best for” labels reflect editorial evaluation, not provider claims

or guaranteed outcomes.

Interest Rates and Overall Cost

We reviewed how lenders structure interest rates and communicate total borrowing costs. Rather than

relying on advertised minimums, we prioritized clarity, competitiveness across borrower profiles, and

lenders' clear explanation of the full cost of a loan.

Fees and Transparency

We examined common fees, such as origination and late fees, and how clearly they are disclosed. Lenders

that explain costs upfront and avoid unclear or excessive charges were viewed more favorably.

Eligibility and Approval Criteria

We assessed how lenders evaluate applicants, including credit score expectations, income verification,

and debt-to-income considerations. Providers with clear and accessible eligibility standards ranked

higher.

Loan Terms and Flexibility

We reviewed available loan amounts, repayment terms, and flexibility options such as early repayment.

Lenders that accommodate diverse financial situations without unnecessary restrictions scored higher.

Customer Experience and Support

We considered application usability, communication quality, and post-funding support. Patterns in

third-party reviews were used to identify consistent strengths or recurring concerns.

Reputation and Stability

We prioritized lenders with an established operating history and consistent consumer feedback, viewing

long-term stability and responsible lending practices as key trust factors.

Community and Consumer Sentiment Research

We also reviewed aggregated discussions from public online communities, including Reddit, to identify

common themes around choosing personal loan lenders. These insights were used solely to provide context

on borrower priorities and pain points, not to verify claims or determine rankings.

Frequently Asked Questions About Personal Loans

How do I get a personal loan fast? The fastest way to get a personal loan is to apply with an online lender

that offers same-day or next-day funding. Make sure your documents are ready to speed up the process.

Do personal loans build credit? Yes, personal loans can build credit when you

make on-time payments. Your payment history is reported to the credit bureaus, which can improve your

score. Missed payments can harm your credit.

How much will a $10,000 loan cost a month? The monthly payment on a $10,000

personal loan depends on your interest rate and the length of your repayment term. Shorter terms have

higher monthly payments but cost less overall. Longer terms reduce the payment but increase the total

interest paid.

What is the interest rate on a personal loan? Personal loan interest rates

typically range from about 6% to 36%, depending on your credit score, income, and the lender. Borrowers

with good or excellent credit usually qualify for the lowest rates, while those with lower credit scores

may pay higher interest rates.

Can I get a personal loan with bad credit? Yes, it is possible to get a personal

loan with bad credit. Some lenders specialize in bad credit personal loans, though interest rates are

usually higher. Improving your credit or applying with a co-signer can help you qualify for better

terms.

Expert Insights by Trevor Smith

Expect higher APRs. Before applying for a personal loan, know

that your rate may be higher because the loan is uncollateralized.

Always compare your options. Never accept the first personal

loan offer you get, since it might not be the best deal.

Personal loans are ideal for smaller expenses. Personal loans

are great for smaller amounts (under $10k) for a minor car repair, while a HELOC is better for

larger expenses like home repairs or remodels.

Watch out for red flags. When comparing your options, watch

out for hidden fees or penalties. You should also be cautious about abnormally high interest rates,

since there is no cap on the rates lenders can charge.

Avoid missing payments. Make sure to never miss a payment on

your personal loan, since it can really hurt your credit.

Best for: Borrowers who want to quickly compare multiple personal loan offers.

LendingTree is an online loan marketplace that connects borrowers with more than 500 personal loan

lenders. Instead of applying with individual lenders one by one, users can submit a single request to

compare multiple personal loan offers in one place. The platform is free to use, and checking potential

offers typically involves a soft credit inquiry, which does not affect your credit score.

Interest rates, loan terms, and fees vary depending on the lender you choose, but LendingTree’s large

network and streamlined comparison process make it a popular choice for borrowers looking to compare

personal loan rates, find competitive offers, and shop lenders efficiently without committing to a hard

credit check upfront.

Best for: Borrowers with good to excellent credit who need a larger loan amount and

want fast funding.

SoFi is a direct online lender that offers personal loans starting at $5,000 with repayment terms of 24

to 84 months. With loan amounts available up to $100,000, SoFi stands out as a strong option for

borrowers who need to finance larger expenses than many other personal loan lenders allow.

Another key advantage is SoFi’s fast funding timeline. Borrowers may be eligible for same-day funding

if they sign the loan agreement by 5:30 PM ET on a business day, though funding speed can vary depending

on the application and verification process. SoFi personal loans generally have minimal fees, but

origination fees may apply and range from 0% to 7%, depending on the loan option selected.

To qualify, borrowers typically need a FICO credit score of good to excellent. Applicants without

strong credit may face higher APRs and may not qualify for SoFi’s lowest advertised rates, making this

lender best suited for well-qualified borrowers seeking competitive terms and larger loan limits.

Best for: Borrowers who want fast prequalification and a relatively streamlined

comparison process.

Credible is an online loan marketplace designed for low-friction rate shopping, allowing borrowers to

get prequalified in about two minutes. Checking rates is free and typically involves a soft credit

inquiry, which does not affect your credit score during the prequalification process.

Unlike larger marketplaces, Credible is known for offering a more streamlined comparison experience,

with borrowers generally less likely to receive a high volume of calls, texts, or emails from multiple

lenders after checking rates. Credible partners with around 20 lenders, and final loan terms—including

APR, fees, and funding speed—will depend on the lender you choose and the completion of a full

application.

Advertised rates (currently 6.49% to 35.99% APR) may include lender discounts for enrolling in autopay

or loyalty programs, where applicable. Actual rates may vary based on the lender’s eligibility criteria,

credit profile, and other underwriting factors.

Disclaimers

BestMoney.com

provides general educational information and comparisons and does not provide financial, legal, or tax

advice. Consider consulting qualified professionals and confirming current terms directly with

lenders/providers.

† Credible Terms and Conditions:

Close with a better rate than you prequalify for on Credible and get a $200 gift card. Terms Apply.

Rates for personal loans provided by lenders on the

Credible platform range between 6.25% - 35.99% APR with terms from 12 to 120 months. Credible also works

with network Partners like MoneyLion and AmONE, who offer loan and other products with different rates

and terms than described here. Rates presented include lender discounts for enrolling in autopay and

loyalty programs, where applicable. Actual rates may be different from the rates advertised and/or shown

and will be based on the lender’s eligibility criteria, which include factors such as credit score, loan

amount, loan term, credit usage and history, and vary based on loan purpose. The lowest rates available

typically require excellent credit, and for some lenders, may be reserved for specific loan purposes

and/or shorter loan terms. The origination fee charged by the lenders on our platform ranges from 0% to

12%. Each lender has their own qualification criteria with respect to their autopay and loyalty

discounts (e.g., some lenders require the borrower to elect autopay prior to loan funding in order to

qualify for the autopay discount). All rates are determined by the lender and must be agreed upon

between the borrower and the borrower’s chosen lender.

For a loan of $10,000 with a three

year repayment period, an interest rate of 7.99%, a $350 origination fee and an APR of 10.43%, the

borrower will receive $9,650 at the time of loan funding and will make 36 monthly payments of $313.32,

assuming your lender deducts the origination fee from the offered loan amount. Assuming all on-time

payments, and full performance of all terms and conditions of the loan contract and any discount

programs enrolled in included in the APR/interest rate throughout the life of the loan, the borrower

will pay a total of $11,279.43.

As of March 3, 2022, none of the lenders on our platform

require a down payment nor do they charge any prepayment penalties.

* LightStream Terms and Conditions:

*Your loan terms, including APR, may differ based on loan purpose, amount, term length, and your credit

profile. Rate is quoted with AutoPay discount. AutoPay discount is only available prior to loan funding.

Rates without AutoPay may be higher. Subject to credit approval. Conditions and limitations apply.

Advertised rates and terms are subject to change without notice.

Payment example: Monthly

payments for a $10,000 loan at 4.99% APR with a term of 3 years would result in 36 monthly payments of

$299.66.

You can fund your loan today

if today is a banking business day, your application is approved, and you complete the following steps

by 2:30 p.m. Eastern time: (1) review and electronically sign your loan agreement; (2) provide us with

your funding preferences and relevant banking information; and (3) complete the final verification

process.

After receiving your loan from us, if you are not completely satisfied with your

experience, please contact us. We will email you a questionnaire so we can improve our services. When we

receive your completed questionnaire, we will send you $100. Our guarantee expires 30 days after you

receive your loan. We reserve the right to change or discontinue our guarantee at any time. Limited to

one $100 payment per funded loan. Truist teammates do not qualify for the Loan Experience Guarantee.

‡ Upgrade Terms and Conditions:

Personal loans made through Upgrade feature Annual Percentage Rates (APRs) of 7.99%-35.99%. All

personal loans have a 1.85% to 9.99% origination fee, which is deducted from the loan proceeds. Lowest

rates require Autopay and paying off a portion of existing debt directly. Loans feature repayment terms

of 24 to 84 months. For example, if you receive a $10,000 loan with a 36-month term and a 17.59% APR

(which includes a 13.94% yearly interest rate and a 5% one-time origination fee), you would receive

$9,500 in your account and would have a required monthly payment of $341.48. Over the life of the loan,

your payments would total $12,293.46. The APR on your loan may be higher or lower and your loan offers

may not have multiple term lengths available. Actual rate depends on credit score, credit usage history,

loan term, and other factors. Late payments or subsequent charges and fees may increase the cost of your

fixed rate loan. There is no fee or penalty for repaying a loan early. Personal loans issued by

Upgrade's bank partners. Information on Upgrade's bank partners can be found at https://www.upgrade.com/bank-partners/.

* Best Egg Terms and Conditions:

*Trustpilot TrustScore as of December 2022. Best Egg loans are personal loans made by Cross River Bank,

a New Jersey State Chartered Commercial Bank, Member FDIC, Equal Housing Lender or Blue Ridge Bank,

N.A., Member FDIC, Equal Housing Lender. The Best Egg Credit Card is issued exclusively by First Bank &

Trust, Member FDIC, Brookings SD pursuant to a license by Visa International. Visa is a registered

trademark, and the Visa logo design is a trademark of Visa International Incorporated. “Best Egg” is a

trademark of Best Egg Technologies, LLC. Offers may be sent pursuant to a joint marketing agreement

between Cross River Bank, Blue Ridge Bank, N.A. and/or First Bank & Trust and Marlette Marketing, LLC, a

subsidiary of Best Egg, Inc.

The term, amount, and APR of any loan we offer to you will

depend on your credit score, income, debt payment obligations, loan amount, credit history and other

factors. Your loan agreement will contain specific terms and conditions. About half of our customers get

their money the next day. After successful verification, your money can be deposited in your bank

account within 1-3 business days. The timing of available funds upon loan approval may vary depending

upon your bank’s policies. Loan amounts range from $2,000– $50,000. Residents of Massachusetts have a

minimum loan amount of $6,500 ; Ohio, $5,001; and Georgia, $3,001. For a second Best Egg loan, your

total existing Best Egg loan balances cannot exceed $100,000. Annual Percentage Rates (APRs) range from

6.99%–35.99%. The APR is the cost of credit as a yearly rate and reflects both your interest rate and an

origination fee of 0.99%– 9.99% of your loan amount, which will be deducted from any loan proceeds you

receive. The origination fee on a loan term 4-years or longer will be at least 4.99%. Your loan term

will impact your APR, which may be higher than our lowest advertised rate.

You need a

minimum 700 FICO® score and a minimum individual annual income of $100,000 to qualify for our lowest

APR. For example: a 5‐year $10,000 loan with 9.99% APR has 60 scheduled monthly payments of $201.81, and

a 3‐year $5,000 loan with 7.99% APR has 36 scheduled monthly payments of $155.12. To help the government

fight the funding of terrorism and money laundering activities, Federal law requires all financial

institutions to obtain, verify, and record information that identifies each person who opens an account.

What this means for you: When you open an account, we will ask for your name, address, date of birth,

and other information that will allow us to identify you. We may also ask to see your driver’s license

or other identifying documents. Best Egg products are not available if you live in Iowa, Vermont, West

Virginia, the District of Columbia, or U.S. Territories.

TO REPORT A PROBLEM OR COMPLAINT

WITH THIS LENDER, YOU MAY WRITE OR CALL– Operations Manager, Email: crt-resolutions@bestegg.com,

Address: P.O. Box 42912, Philadelphia, PA 19101, Phone: 1-855-282-6353. This lender is licensed and

regulated by the New Mexico Regulation and Licensing Department, Financial Institutions Division, P.O.

Box 25101, 2550 Cerrillos Road, Santa Fe, New Mexico 87504. To report any unresolved problems or

complaints, contact the division by telephone at (505) 476-4885 or visit the website https://www.rld.nm.gov/financial-institutions/

* Achieve Terms and Conditions:

1. Home Equity loans are available through Achieve Loans (NMLS ID #227977), Equal Housing Lender. All

loan requests are subject to eligibility requirements, application review, loan amount, loan term, and

lender approval. Product terms are subject to change at any time. Home loans are a line of credit.

Loans are not available to residents of all states and available loan terms/fees may vary by

state where offered. Line amounts are between $15,000 and $300,000 and are assigned based on

debt-to-income ratio and loan-to-value ratio. Minimum 640 credit score applies for debt consolidation

requests, minimum 670 applies for cash out requests.

Fixed rate APRs range from 6.74% -

14.75% and are assigned based on underwriting requirements and offer APRs include a .50% discount for

automatic payment enrollment (autopay enrollment is not a condition of loan

approval).

Example: average HELOC is $57,150 with an APR of 12.75% and estimated monthly

payment of $951 for a 15-year loan. 10-year and 15-year terms available. Both terms have a 5-year draw

period with the remaining term being a no draw period. Payments are fully amortized during each period

and determined on the outstanding principal balance each month. Closing fees range from $750 to $6,685,

depending on line amount and state law requirements and typically include origination (2.5% of line

amount) and underwriting ($725) fees if allowed by law.

Property must be owner-occupied and

combined loan-to-value ratio may not exceed 80%, including the new loan request. Property insurance is

required and flood insurance may be required if the subject property is located in a flood zone. You

must pledge your home as collateral.

Average funding time is between 15 to 18 days from

submitted application and documentation and includes rescission. Contact Achieve Loans for further

details.

* Reach Financial Terms and Conditions:

All loans are subject to eligibility criteria and review of creditworthiness and history. Terms and

conditions apply. All loans advertised are unsecured personal loans issued by either Metabank® National

association, member FDIC, or FinWise Bank, a Utah chartered commercial bank, member FDIC, as creditor,

on the Liberty Lending platform. If you are approved for a loan, the interest rate offered will depend

on your credit profile, your application, and the loan term you select. Fixed Annual Percentage Rates

(APR) range from 5.99% to 35.99%. You could receive a loan of $10,000 with an interest rate of 8.93%, an

origination fee of $200, for an APR of 9.80%, which would result in total payment of $12,435 with 60

monthly payments of $207.20. Your actual rate may differ and depends on your credit history, loan

amount, and term. Total approved loan amount reflects origination fee, which ranges from 0% to 5%.

*Within 24 hours of your loan approval, loan proceeds will be available to pay the creditors named on

your Truth-In-Lending Disclosure.

* Universal Credit Terms and Conditions:

Personal loans made through Universal Credit feature Annual Percentage Rates (APRs) of 11.69%-35.99%.

All personal loans have a 5.25% to 9.99% origination fee, which is deducted from the loan proceeds.

Lowest rates require Autopay and paying off a portion of existing debt directly. Loans feature repayment

terms of 36 to 60 months. For example, if you receive a $10,000 loan with a 36-month term and a 28.47%

APR (which includes a 22.99% yearly interest rate and a 7% one-time origination fee), you would receive

$9,300 in your account and would have a required monthly payment of $387.05. Over the life of the loan,

your payments would total $13,933.62. The APR on your loan may be higher or lower and your loan offers

may not have multiple term lengths available. Actual rate depends on credit score, credit usage history,

loan term, and other factors. Late payments or subsequent charges and fees may increase the cost of your

fixed rate loan. There is no fee or penalty for repaying a loan early. Personal loans issued by

Universal Credit's bank partners. Information on Universal Credit's bank partners can be found

at https://www.universal-credit.com/bank-partners/.

* LendingClub Terms and Conditions:

Between Jan 2025 to June 2025, 55% of LendingClub Personal Loans that were approved for funding (which

is after your loan application is approved) on a given business day were disbursed within 24 hours.

Actual availability of funds may vary and is dependent on multiple factors, including, but not limited

to your receiving bank’s processing times and policies. A business day is defined as Monday through

Friday and excludes the weekend and bank holidays.

A representative example of payment terms

for a Personal Loan is as follows: a borrower receives a loan of $17,413 for a term of 36 months, with

an interest rate of 12.49% and a 6.00% origination fee of $1,045 for an APR of 16.86%. In this example,

the borrower will receive $16,369 and will make 36 monthly payments of $582. Loan amounts range from

$1,000 to $50,000 and loan term lengths range from 24 months to 72 months. Some amounts, rates, and term

lengths may be unavailable in certain states.

For Personal Loans, APR ranges from 7.90% to

35.99% and origination fee ranges from 0.00% to 8.00% of the loan amount. APRs and origination fees are

determined at the time of application. Lowest APR is available to borrowers with excellent credit.

Advertised rates and fees are valid as of April 22, 2025 and are subject to change without

notice.

Loans are made by LendingClub Bank, N.A., Member FDIC, Equal Housing Lender

(“LendingClub Bank”), a wholly-owned subsidiary of LendingClub Corporation, NMLS ID 167439. LendingClub

Bank is not an affiliate of Natural Intelligence, which is an unrelated third party (“third party”).

LendingClub Bank is not responsible for any products and services provided by this third party. Credit

eligibility is not guaranteed. Loans are subject to credit approval and may be subject to sufficient

investor commitment. Credit union membership may be required. Certain information that LendingClub Bank

subsequently obtains as part of the application process (including but not limited to information in

your consumer report, your income, the loan amount that your request, the purpose of your loan, and

qualifying debt) will be considered and could affect your ability to obtain a loan. Loan closing is

contingent on accepting all required agreements and disclosures at LendingClub.com. “LendingClub” and

the “LC” symbol are trademarks of LendingClub Bank.

* OneMain Financial Terms and Conditions:

You must complete a loan application and continue to meet any criteria used to select you for a loan

offer. Not all applicants are approved. Loan approval and actual loan terms depend on applicant’s state

of residence and ability to meet OneMain Financial credit standards such as a responsible credit

history, sufficient income after monthly expenses, and if applicable, availability of eligible

collateral. Not all approved applicants qualify for larger loan amounts, lower APRs, or

the most favorable loan terms. For example, larger loan amounts typically require a first lien on a

motor vehicle that is no more than ten years old, meets our value requirements, and is titled in

applicant’s name with valid insurance. APRs are generally higher on loans not secured by a vehicle.

Example Loan: A $6,000 loan with a 24.99% APR that is repayable in 60 monthly installments would have

monthly payments of $176.07. OneMain charges origination fees allowed by law. Depending on

the state where the loan is opened, the origination fee may be either a flat amount or a percentage of

the loan amount. Flat fees vary by state, ranging from $25 to $500. Percentage-based fees vary by state,

ranging from 1% to 10% of the loan amount subject to certain state limits on the fee amount. For

information about these fees and minimum and maximum loan sizes available in certain states, visit

omf.com/loanfees. Current OneMain Customers: Loan offers presented to a consumer assume

the individual has no active loan with OneMain or one of its affiliates. If a customer applies for a new

loan offer, a OneMain representative will discuss available options. Active-duty military,

their spouse or dependents covered by the Military Lending Act (MLA) may not pledge any vehicle as

collateral. If you are covered by the MLA, you are not eligible for secured loans. Loan

proceeds cannot be used for postsecondary educational expenses as defined by the CFPB’s Regulation Z

such as college, university or vocational expense; for any business or commercial purpose; to purchase

cryptocurrency assets, securities, derivatives or other speculative investments; or for gambling or

illegal purposes. Time to Fund Loans: Funding within one hour after loan closing through

SpeedFunds® must be disbursed to a bank-issued debit card. Disbursement by check or ACH may take up to

1-2 business days after closing.

* Splash Financial Terms and Conditions:

Splash Financial, Inc. (NMLS # 1630038) Terms and conditions apply. Products may not be available in

all states. The information you provide to us is an inquiry to determine whether Splash’s lending

partners can make you a loan offer, but it does not guarantee you will receive any loan offers. Splash

marketplace offers rates between 10.24% to 26.39% APR. Rates are subject to change without notice. Not

all applicants qualify for the lowest rate.

The lowest rates are reserved for the most

creditworthy applicants and depend on credit score, loan term, and other factors. Personal loans offered

through Splash may have an origination fee up to 7.49% which may be deducted from the loan

proceeds.

Lowest rates may require AutoPay and may require paying off a portion of existing

debt directly. The AutoPay discount requires you to agree to make monthly principal and interest

payments by an automatic monthly deduction from a savings or checking account. The AutoPay discount will

not be applied if AutoPay is not in effect. See the loan agreement for details.

Personal

loans are solely for personal, family, or household purposes and may not be used to purchase or

refinance real estate, securities, or other investments. Personal loans may not be used for business

purposes, to finance post-secondary education expenses, for short-term bridge financing, or for any

illegal purpose.

¹ To check the rates and terms you qualify for, Splash Financial conducts a

soft credit pull that will not affect your credit score. However, if you choose a product and continue

your application, the lender will request your full credit report from one or more consumer reporting

agencies, which is considered a hard credit pull and may affect your credit.

²Loans feature

repayment terms of 24 to 60 months. For example, if you receive a $10,000 loan with a 36-month term and

a 17.98% APR (which includes a 14.32% yearly interest rate and a 5% one-time origination fee), you would

receive $9,500 in your account and would have a required monthly payment of $343.33.

³ Once

you have successfully completed the loan application process, it typically takes one to two business

days to receive funds. However, funding may take up to two weeks.

* Santander Bank Terms and Conditions

Personal Loans are subject to individual approval and meeting our credit standards. Your primary

residence must be located in AZ, CA, CT, CO, DC, DE, FL, GA, IL, IN, MA, MD, ME, MI, MN, MO, NC, NJ, NH,

NY, OH, OR, PA, RI, TN, TX, VA, VT, or WA. The fixed loan Annual Percentage Rate (APR) will depend on

your creditworthiness and use of automatic payments (ePay) from any deposit account. The APR on a

Personal Loan will increase by 0.25 percentage points and the payment will increase, if ePay is not

elected or is discontinued. Fixed loan APRs (with ePay) range from 7.99% to 24.99% and are subject to

change without notice. Loan amounts range from $5,000 to $50,000. Loan repayment terms range from 36

months to 84 months. All terms are subject to change without notice. Personal Loans cannot be used to

finance post-secondary educational expenses.

Personal Loan Monthly Payment Example: For a

personal loan of $20,000 with a 60-month term at 15.49% APR, the monthly payment amount is approximately

$480.96 to repay your loan in 60 payments. This example is an estimate only and assumes all payments are

made on time.

Based on the time your application is received, same-day funding is available

in many cases, depending on your creditworthiness and the funding instructions you

provide.

Santander Bank, N.A. All rights reserved. Santander, Santander Bank and

the Flame logo are trademarks of Banco Santander, S.A. or its subsidiaries in the United States or other

countries. All other trademarks are the property of their owners.

* SoFi® Terms and Conditions:

Terms and conditions apply. SOFI RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS

AND BENEFITS AT ANY TIME WITHOUT NOTICE. To qualify, a borrower must be a U.S. citizen or other eligible

status, be residing in the U.S., and meet SoFi's underwriting requirements. Not all borrowers

receive the lowest rate. Lowest rates reserved for the most creditworthy borrowers.If approved, your

actual rate will be within the range of rates at the time of application and will depend on a variety of

factors, including term of loan, evaluation of your creditworthiness, income, and other factors. If SoFi

is unable to offer you a loan but matches you for a loan with a participating bank, then your rate may

be outside the range of rates listed above. Rates and Terms are subject to change at any time without

notice. SoFi Personal Loans can be used for any lawful personal, family, or household purposes and may

not be used for post-secondary education expenses. Minimum loan amount is $5,000. The average of SoFi

Personal Loans funded in 2024 was around $33K. Information current as of 02/23/26. SoFi Personal Loans

originated by SoFi Bank, N.A. Member FDIC. NMLS #696891 (http://www.nmlsconsumeraccess.org/ and state restrictions). See http://sofi.com/legal for state-specific license

details. See http://sofi.com/eligibility for

details

Fixed rates from 8.74% APR to 35.49% APR. APR reflect the 0.25% autopay interest rate

discount and a 0.25% SoFi Plus interest rate discount. SoFi Platform personal loans are made either by

SoFi Bank, N.A. or , Cross River Bank, a New Jersey State Chartered Commercial Bank, Member FDIC, Equal

Housing Lender. SoFi may receive compensation if you take out a loan originated by Cross River Bank.

These rate ranges are current as of 02/04/26 and are subject to change without notice. Not all rates and

amounts available in all states. See SoFi Personal Loan eligibility details at personal http://sofi.com/eligibility. Not all applicants

qualify for the lowest rate. Lowest rates reserved for the most creditworthy borrowers. Your actual rate

will be within the range of rates listed above and will depend on a variety of factors, including

evaluation of your credit worthiness, income, and other factors.

Loan amounts range from

$5,000– $100,000. The APR is the cost of credit as a yearly rate and reflects both your interest rate

and an origination fee of 9.99% of your loan amount for Cross River Bank originated loans which will be

deducted from any loan proceeds you receive and for SoFi Bank originated loans have an origination fee

of 0%-7%, will be deducted from any loan proceeds you receive.

Autopay: The

SoFi 0.25% autopay interest rate reduction requires you to agree to make monthly principal and interest

payments by an automatic monthly deduction from a savings or checking account. The benefit will

discontinue and be lost for periods in which you do not pay by automatic deduction from a savings or

checking account. Autopay is not required to receive a loan from

SoFi.

SoFi Plus Discount: SoFi Plus members are eligible for an

interest rate reduction of 0.25% on a Personal Loan. To be eligible for the discount, you must meet the

SoFi Plus eligibility criteria within 31 days of the funding of your loan. For complete SoFi Plus

eligibility, please see the SoFi Plus terms. When you enroll in SoFi Plus, the discount will lower the

interest rate that applies to your loan only during periods in which you are enrolled in SoFi Plus. The

discount will be removed during periods in which SoFi determines you are not enrolled in SoFi Plus. Each

time your loan is re-amortized, your monthly payment amount will change based upon the interest rate

that was in place. SoFi reserves the right to change or terminate this offer for unenrolled participants

at any time. You are not required to enroll in SoFi Plus to be eligible for Loan

approval.

¹Borrow Better Week Rate Drop: Additional terms and

conditions apply. Limited time 0.50% BPS rate drop for new Personal Loan, Student Loan Refinancing,

Private Student Loan, and Home Equity Loan applications started between 3/17/26 – 3/23/26 and is subject

to lender approval. Promotion does not include Home Loan purchase, refinance, or HELOC applications. To

receive the discount, you must start a loan application with SoFi between 3/17/26 and 3/23/26 at 11:59PM

PST and meet SoFi’s underwriting criteria.